The latest version of RangeBars PRO & Renko PRO plug-ins includes an additional option in the CSV2FXT script mods – StrategyQuantExport. When enabled, the scripts create a proprietary CSV file, which is compatible with the latest StrategyQuant products. As of version 3.6, StrategyQuant adds support for renko & range bar charts, which enable creating a whole new class of strategies that would not be possible with regular time based charting.

To begin using RangeBar & Renko data with StrategyQuant, you first need to convert tick data into Range/Renko bars using CSV2FXT script mods with StrategyQuantExport set to true and import this data into StrategyQuant’s Data Manager.

It is wise to create a number of different bar sizes for various instruments and import this data into StrategyQuant’s Data Manager for later use.

To import the created data files, you need to go to the Data Manager tab in StrategyQuant, add new symbol(s) and populate them with data. The process is very simple and only requires a few basic steps.

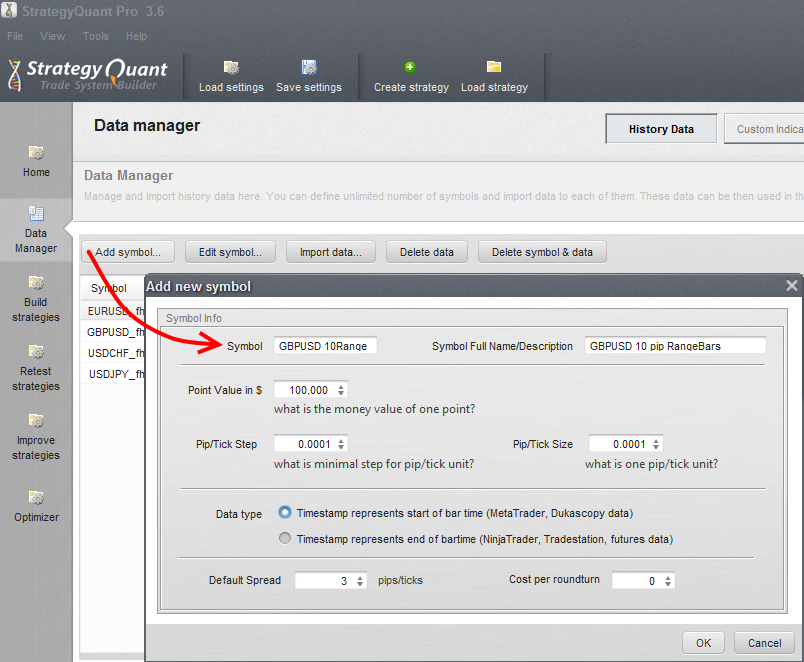

Start with Add symbol…

First, type in the Symbol name and remember to use names that will pass all the relative information and enable you to quickly identify the chart you want to use in the strategy building process. For example, you can choose GBPUSD_10Range to label a 10 pip RangeBar chart of GBPUSD. Once you have that done, make sure that you select the Data type as “Timestamp represents start of bar time (MetaTrader, Dukascopy data)” and that you set the remaining fields according to your chosen instrument. When done click OK to save the symbol.

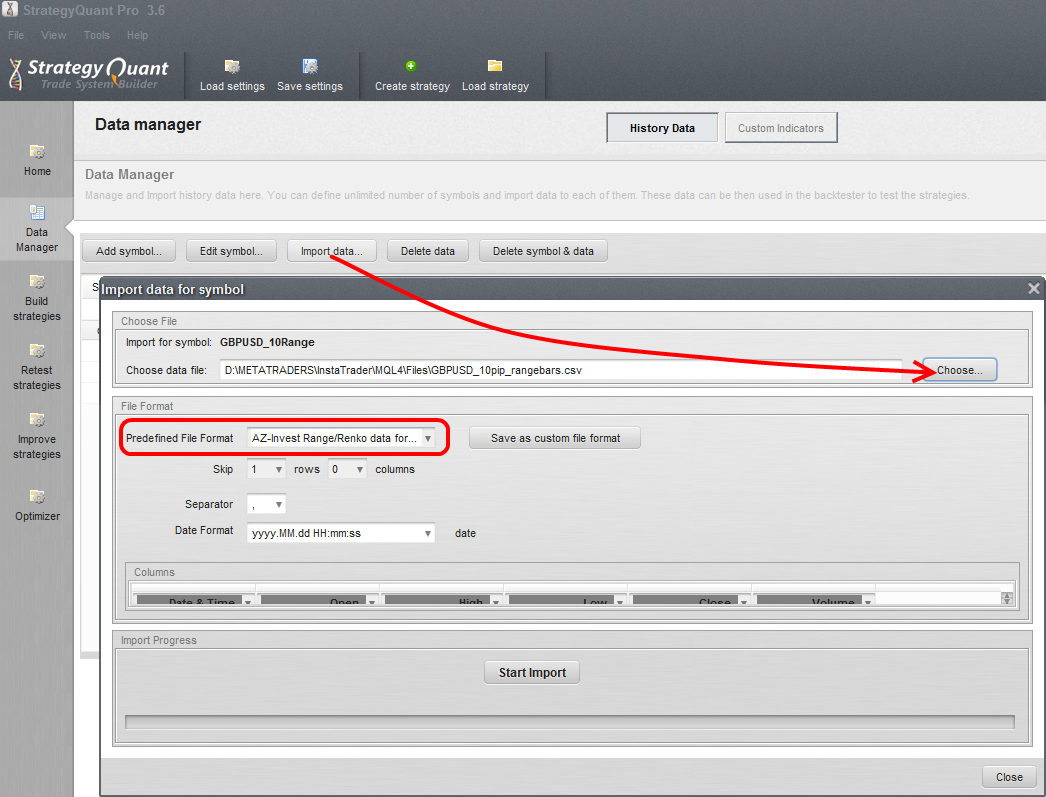

Now it is time to populate the symbol’s record with data exported by the CSV2FXT script for Renage or Renko (depending on the type of chart data you wish to import). This is done by pressing Import data.. for the selected symbol.

The Predefined File Format needs to be “AZ-Invest Range/Renko data format” and you need to select the correct CSV file. Once the file is chosen, press Start Import.

CSV2FXT script mods will use the following naming convention to simplify locating the file you need: XXXYYY_ZZpip_BARTYPE, where XXXYYY is the symbol name, ZZ will be set to the barSize setting chosen in CSV2FXT and BARTYPE will be either range bars or renko.

When the process is finished you will see the new symbol with Intraday timeframe and imported data time span along with selected symbol properties.

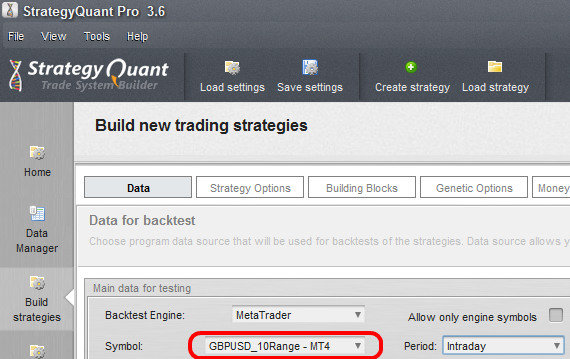

At this point, you can move on to strategy building, where you need to choose the selected range/renko chart as your data for testing. This is done in the Settings / Data tab of Build Strategies by selecting the desired symbol.

The rest of the strategy building process is exactly the same as with regular time-based charts.

APR

2014